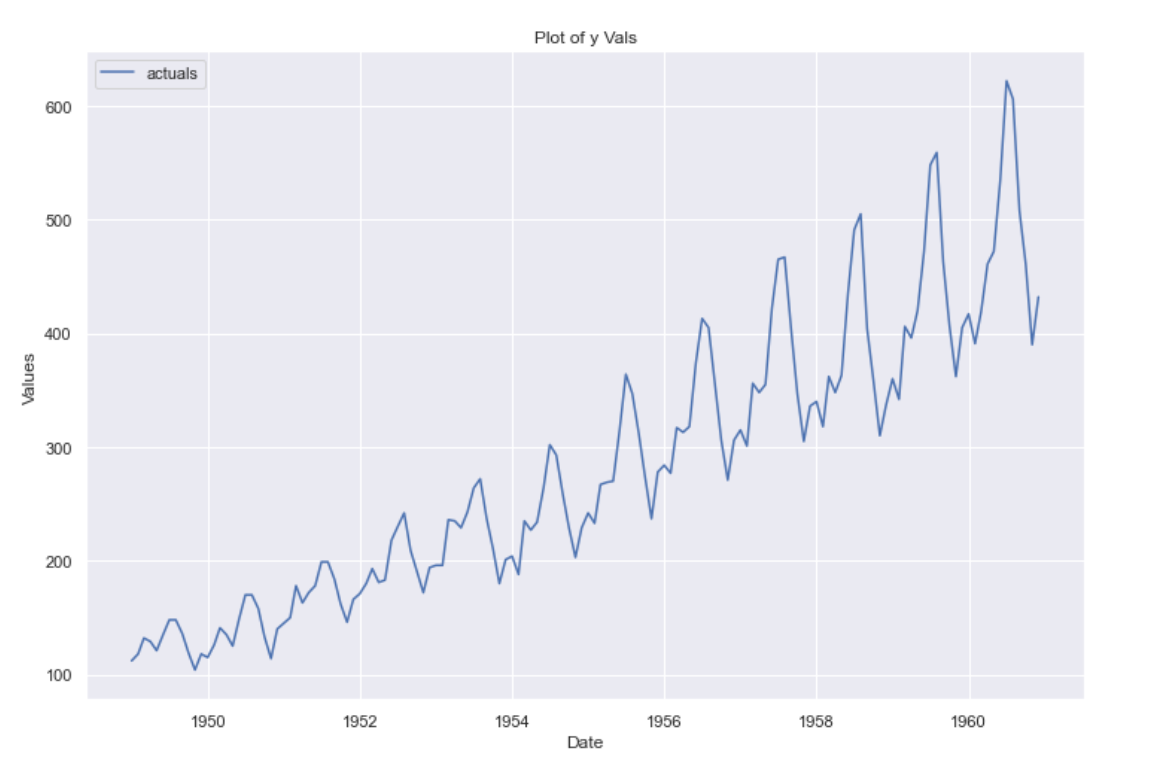

When analyzing a Time Series, we often use Decomposition in Time Series to separate it into three main components:

- Trends in Time Series – long-term direction in the data

- Seasonality in Time Series – repeating patterns at fixed intervals

- Residuals Analysis – the unexplained variation after removing trend and seasonality

A common method for decomposition is STL Decomposition, which flexibly extracts trend and seasonal components.

Why Decompose?

- Helps identify stable trend and seasonal structures.

- Makes it easier to test whether the series is a Stationary Time Series (constant mean and variance).

- Prepares the data for forecasting models.

Handling Trend and Seasonality

To model effectively, you often need to make the data stationary:

- Remove trends

- Remove seasonality

This can be checked using:

- Plots of the series

- ACF Plots and PACF Plots

- Statistical tests (e.g., ADF test)

Practical Considerations

- Check stationarity before modeling Stationary Time Series.

- Split into components (trend, seasonality, residuals) where helpful.

- Avoid over-differencing — too much differencing removes useful information.

- Model choices:

- Classical approaches: SARIMA, Exponential Smoothing

- Decomposition + ML: Random Forest for Time Series, Gradient Boosting

Resource: Understanding Stationarity in Time Series

Image